One of the things that you need to do while planning for retirement is determining how long you expect your retirement to last.

True, that’s easier said than done; predicting how long you will live as a retiree is not just dreadful, but also very easy to get wrong. What if you end up living longer than your retirement fund lasts?

You clearly cannot afford to get this wrong. You might end up with no money at a very old age or have to live with less than you expected as time goes on. Both scenarios are more dreadful than predicting when you will die.

But what are you supposed to do about that? Well, let’s see…

Why Life Expectancy Tables Don’t Work

Many financial advisors rely on life expectancy tables to create your retirement plan.

For example, the average Canadian lives to 82, so assuming that you will live that much and not longer makes sense. Or does it?

You see, you may not be the average Canadian. Are you ready to risk your retirement life on that assumption?

Assuming your life span based on statistical probability is very risky when there are so many parameters that will influence how long you live.

So, counting on life expectancy tables is out of the question…

What to Do Instead

Here are two alternatives:

- Assume that you will live for a very long time (20+ above the average) unless your medical history makes that very unlikely

- Assume an average age, but make sure that by the time you retire you have fully paid for your house so you can rely on selling it or getting a reverse mortgage if you end up outliving your fund

In other words, either apply a “margin of safety” by assuming a very long life or get “insurance” in case you end up being an outlier.

If you go with the first option, then all that remains is for you to determine your optimal drawdown plan. To do that you will either need a financial advisor or software that guides you through the process.

For the DIY types, a great solution is Wealthica’s power-up Wealthscope Jubilee. It’s post-retirement drawdown planning tool will help you leave nothing to chance when it comes to your retirement.

Of course, to have a drawdown plan, you need to make sure your contributions are adequate to match your needs in retirement. Wealthica’s registered contribution widget will help you keep an eye on how much you are contributing to your registered accounts.

Ensure that you retire the right way by Signing Up to Wealthica to get access to it!

Oh, one more thing…

Plan C – Don’t Touch the Goose!

Before you go, there’s another solution. But it’s not for everyone.

You could eliminate the need to predict your life’s length if you accumulated enough wealth, invested in a conservative portfolio, and lived off the yield that it provides (after accounting for inflation).

First, that requires a more than decent income and bigger contributions. Second, it requires a wise portfolio construction to ensure an adequate yield and the safety of principal. A financial planner may be of help in the latter.

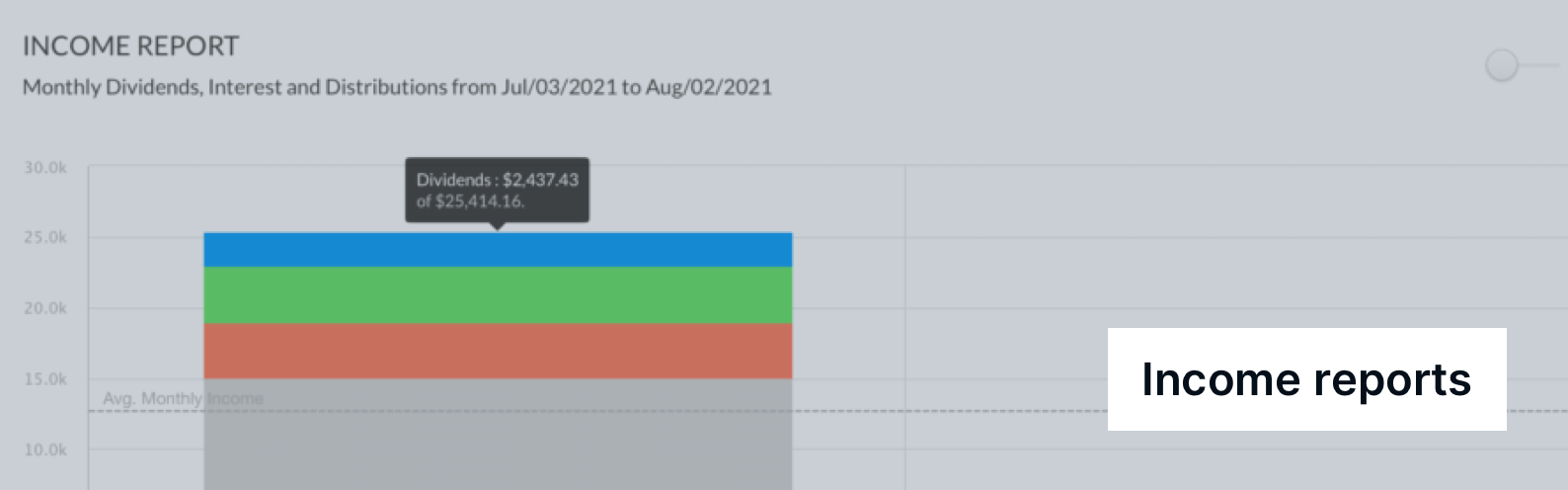

Wealthica can also help you with getting a clear idea of how much income you are getting from your investments. Use the income power-up to see dividends, distributions and interest income you are getting across all your accounts.

You can use Wealthica to keep track of your investment performance and ACB so when you realize gains, you are sure of the returns and make tax advantageous decisions.

On top of that, if you have the zeal to learn how to create and manage a portfolio by yourself, then Wealthscope Jubilee will help you get the job done. Within Wealthica’s power-up, you will be able to create a custom portfolio or answer relevant questions to let the tool create it for you.

Wealthica has a host of tools that can help you on your journey to retirement.

Sign up to Wealthica today and get access to retirement tools, budget solutions, net worth aggregating, and more!